|

|

|

|

|

|

|

|

|

|

Position Sizing as Risk Control (Where Outcomes Are Actually Determined)

What comes to mind when you think of risk in your portfolio?

|

Most investors are used to thinking of risk in terms of volatility. This makes sense in some ways since a highly volatile stock can makes you doubt your thesis at times and can making a good night sleep harder to come by. However, volatility is not the type of risk an investor should be concerned with.

|

The only risk that matters for your portfolio is the risk of ruin.

|

A well constructed portfolio has assets with high expected returns over time. But these are volatile assets. You come close to staring "risk of ruin" in the face, if a large number of your holdings move down at the same time. If these assets are a large portion of your portfolio, the risk is larger. If you are using leverage, the risk can be existential.

|

You can get wiped out despite owing great stocks, if you do not pay attention to your position sizes.

|

Why Stock-Level Risk Thinking Is Incomplete

In the past I have been forced to sell a stock even when I believed in the thesis. The position size become untenable. This has likely happened to you as well.

|

|

Stocks are volatile. There is no such thing as a safe stock. I remember when Proctor and Gamble stock, the bluest of the blue chip, was cut down by half overnight after an earnings report. UPS is a more recent example. Exiting Amazon business is the correct strategic move, but investors with shorter term outlook have punished the stock. If one of these stocks formed a significant part of your portfolio, and even when you believed in the long term outlook, you would have still suffered.

|

But if your position was sized appropriately, you would survive. And surviving is a pre-requisite to success.

|

Most portfolios blow up due to sizing errors, not because they own bad stocks.

|

Position Sizing vs. Diversification (A Critical Distinction)

Am I talking about diversification in a different way?

|

Depends. Diversification is important to reduce portfolio volatility but it is just one part of the equation. Position sizing spreads the exposure, similar to diversification, and it also sizes the positions so the stocks with greatest potential get higher allocation.

|

In short, it optimizes returns/risk.

|

The Hidden Ways Investors Oversize Risk

Today's investors in the S&P 500 index funds are unknowingly betting 35% of their portfolio in just 7 stocks. Worse, these 7 stocks expose you to the same sector, so if there was a sector wide decline, the so called highly diversified index and the fund will sink your portfolio.

|

High conviction tech positions like Nvidia and Amazon have been dominating portfolios in the recent years. For many, these positions have grown over the years to dominate the portfolio. Along with this growth, there has been a growth in risk exposure to the tech sector, more specifically AI. Investors today are happy as the recent performance has been phenomenal and many expect this performance to continue. But how long will this last?

|

Even if this is not you, you need to be aware of the following:

|

- “High-conviction” positions that quietly dominate the portfolio

- Letting winners grow without reassessing risk

- Correlated positions masquerading as diversification

- Emotional sizing driven by recent performance

These creep on to you if you are not careful. The best way to manage this is to have a process with a portfolio review on a cadence.

|

Position Sizing as a Survival Mechanism

I briefly touched upon this earlier. Buffett has said that Rule #1 of investing is "Do Not Lose Money". When you are in a drawdown, your options suddenly get limited. Discipline gets shaky and you are likely to exit your positions at the worst possible moment.

|

|

Did you know that most fund investors underperform the funds that they have invested in?

|

This strange outcome is the result of investors "tweaking" their portfolios by selling when they are scared and buying more when they are happy. They add more exposure when their exposure is already elevated, and they reduce exposure when they should be adding. Of course, sometimes this becomes a necessity as the position was not sized properly to begin with.

|

Proper position sizing discipline helps you avoid counter productive actions, which in turn means you have greater staying power, better discipline and more rational and controlled management of your portfolio.

|

Why Position Sizing Matters Even More in Small-Cap Value

Small cap value stocks give you higher performance. This comes with the cost of higher volatility. If you can't handle volatility, you will be wiped out - either through your own actions or through forced liquidations due to margin calls. Improper position sizing will turn opportunity into regret.

|

The position sizing method you choose will require you to limit exposure to any one asset based on that particular assets attributes such as volatility, expected returns or ATR. This will lead you to own multiple stocks in the portfolio, ensuring your portfolio is diversified. You may argue that this will dampen your portfolio returns. I suggest that this ensures your portfolio lasts full business cycles which will allow it to capture the full alpha that exists because of your superior stock selection.

|

From Stock Picking to Risk Budgeting

Equal weighting is a start. Although better than the market cap weighting the most investors use when they buy a typical index fund, this doesn't account for the fact that different stocks are differently volatile and have different return expectations.

|

I personally have considered and used 2 different systems. Risk Parity, and Kelly Criterion. I will lay out a conceptual description of these systems and we can go into more detail in the future editions of the newsletter.

|

Risk Parity Portfolio Sizing System: Uses ATR (Average True Range) as a proxy for "risk". You can pick a multiple of ATR as the maximum draw down level that you are comfortable with, beyond which you will exit the stock. For example, if you decide to limit your drawdowns to 3xATR, this is the exact monetary value you are risking for that stock. Then you can decide that you will limit each stock loss to a maximum of 1% (you can choose 2% or even 3% if you want to be more aggressive, or 0.5% if you want to be less aggressive). This choice will tell you how many shares you should buy. In this example,

|

1% of your portfolio value = 3 x ATR/share x number of shares, which can then be solved to give you your position size.

|

This will equalize the risk of loss across all your positions in nominal value. Which means, you will buy less of more volatile stocks and more of less volatile stocks.

|

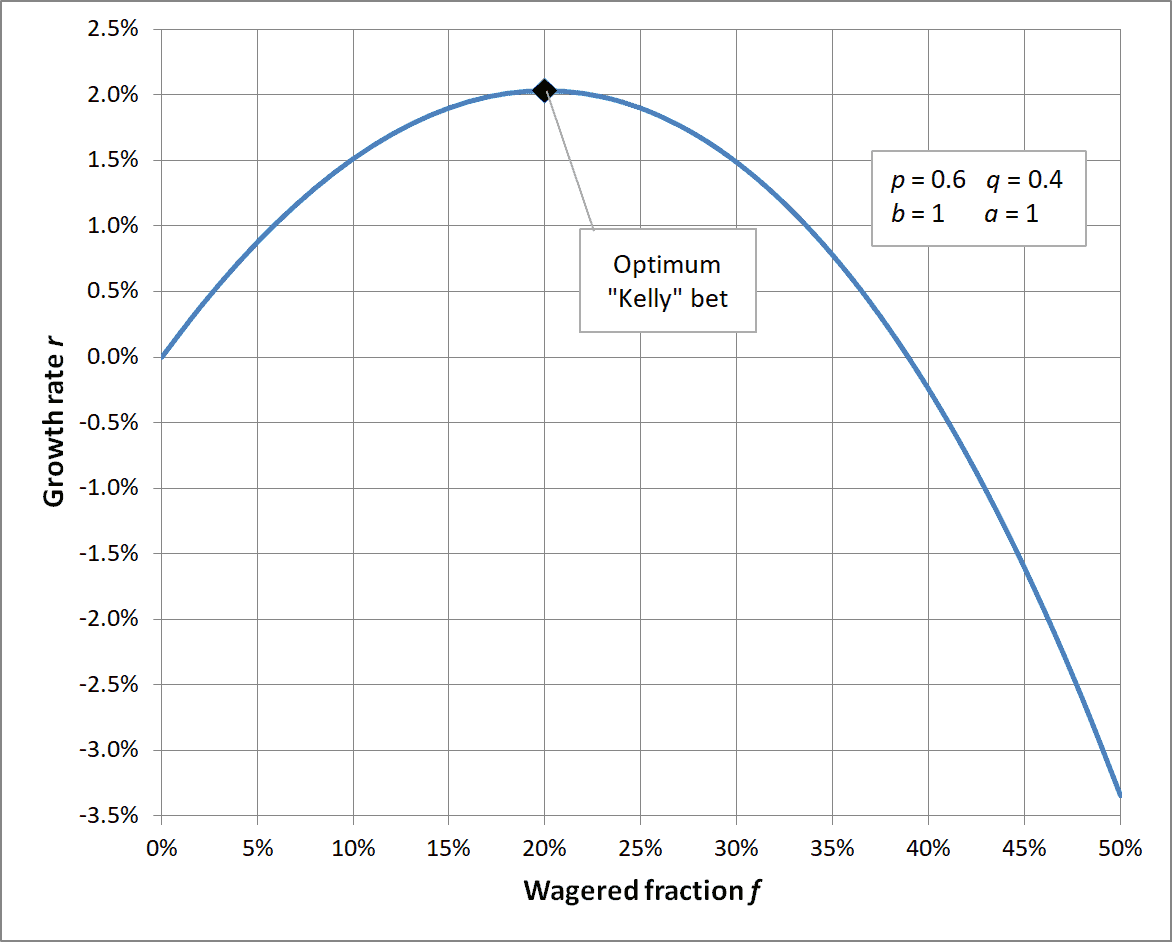

Kelly Criterion: Uses expected returns and volatility of each stock to calculate the position size. Typically used for single bet systems, it can be adapted to multi stock portfolio by including stock correlations. If you can master the math, this will optimize your portfolio for high growth while eliminating the risk of ruin altogether.

|

Kelly Criterion forces you to invest more in stocks with higher expected returns and lower volatility. It also ensures you will fill the portfolio with stocks that are uncorrelated of very lightly correlated, this giving you the maximum benefits of diversification with minimum number of positions (so the expected returns are higher).

|

So which method is better? It is the one that you use. The biggest destroyer of portfolios by far is a lack of position sizing process. When you institute a process, it forces you to pay attention to those attributes of your portfolio that ultimately determine your performance.

|

Foundational Reading (Website Articles)

Closing: What Comes Next

In the next issue we will discuss rebalancing and return harvesting. Keep in mind that position sizing is not a one time effort. This is an ongoing process and the portfolios need to be reassessed as expected returns change, and volatility and correlations evolve. If you do not do this, you will once again end up with a lop-sided and risk heavy portfolio.

|

|

|

|

|

|

|

|

|

|

|

|

|

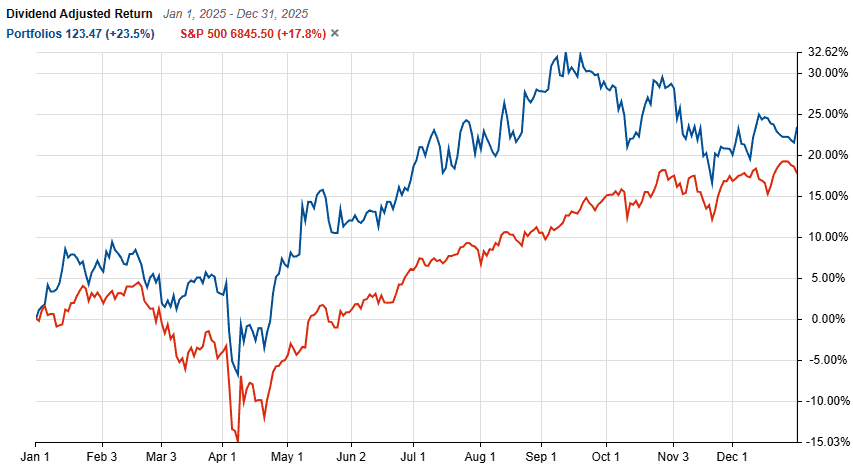

Inner Circle Portfolio Performance

|

|

|

The portfolio performance is updated once a month, and tracked YTD until the end of the prior month. Performance is tracked as time weighted total return.

|

|

|

|

|

|

Upgrade to Inner Circle

- My actual Small Cap Value portfolio with highly profitable but under followed stocks and Kelly Criterion optimized weights

- Detailed investment thesis for portfolio stocks, including target prices and expected returns emailed to you as soon as published

- 1 year membership with NO auto-renewal. Repurchase membership again if you wish to continue for another year once your term completes.

|

|

|

|

|

|

|

|

|

Managing Drawdowns: How I Protect Capital Without Losing Upside

|

|

|

|

In 2008, one of my portfolio positions fell 67% in four months. I had bought a small industrial company with a clean balance sheet, a long operating history, and what I thought was a conservative valuation. Then the financial crisis hit, credit markets froze, and customers stopped ordering. The stock went from $18 to $6 in the time it takes …

|

|

|

|

|

|

|

|

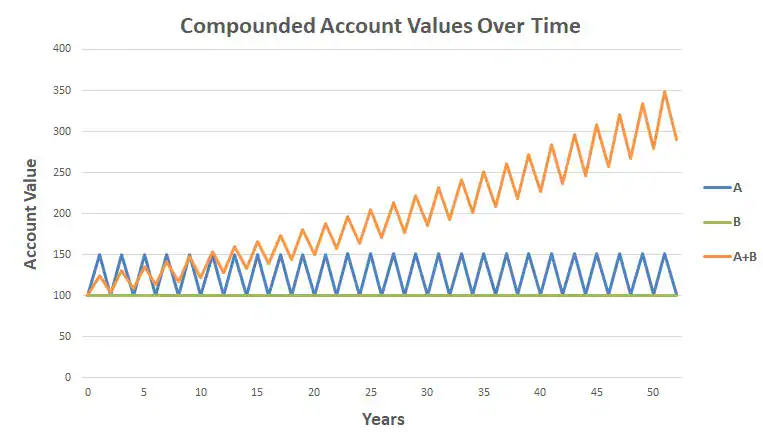

Shannon's Demon Explained: Why Rebalancing Beats Buy-and-Hold Over Time

|

|

|

|

I want to tell you about one of the most counterintuitive ideas in all of investing, an idea so strange that when I first encountered it, I spent about an hour with a spreadsheet trying to convince myself it was wrong before I finally accepted that it was right. It is called Shannon's Demon. And once you understand it, you …

|

|

|

|

|

|

|

|

Full Kelly vs. Fractional Kelly: Which Position Sizing Approach Is Right for You?

|

|

|

|

Most investors spend enormous effort deciding which stocks to buy and almost no effort deciding how much to buy. That is exactly backwards. In the long run, position sizing will have as much impact on your returns as stock selection and it will have more impact on your survival as an investor. I use the Kelly Criterion as the mathematical …

|

|

|

|

|

|

|

|

|

|

|

|

|