|

|

|

|

|

|

|

|

|

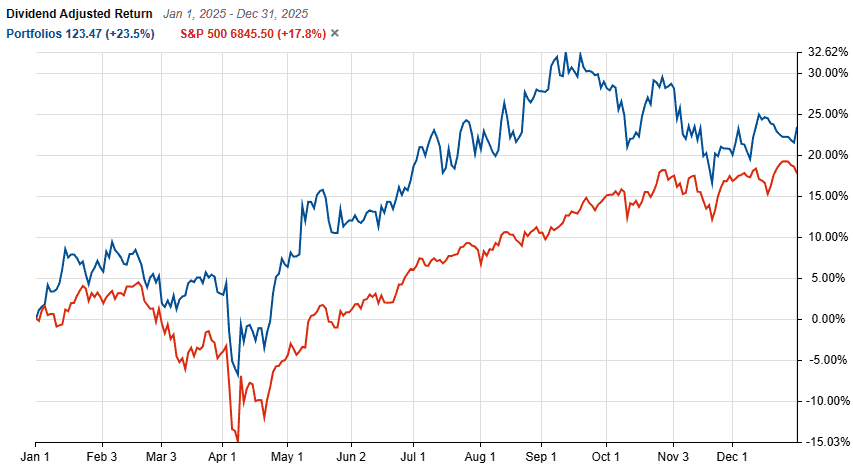

We have returned close to 6% ABOVE the S&P 500 for 2025.

|

We generally have had a portfolio with very little turnover. The portfolio is mostly made up of small names in boring industries and they have held up well. Interestingly, the portfolio never really dipped below the market performance all year last year.

|

What is 23.5% annual return (TWR), when you have so many investors returning 100%+ for the last year?

|

This is certainly a problem I face every single year. There are always people who do spectacularly well, leaving me behind in dust for that year. I don’t mind.

|

Value investing is about discipline and process and the results come over time. My goal is to generate consistent market beating returns every year. And, not to lose money in any year. With time and compounding, this creates significant wealth, without all the exciting and wild performance swings.

|

My Thoughts on the Market Today

We just ended a strange year and the new year is now getting stranger.

|

I have been watching the precious metal markets, with gold and silver breaking new all time highs seemingly every trading day. The geo political environment may have some impetus for the investors to seek out safe havens, but a lot of this is also driven by the enormous demand for metals and commodities, and many other rare earth minerals, to support the epic levels of data center construction around the globe to support new AI models and future AI demand.

|

|

As I have said earlier, we are in an AI bubble. I repeat it here because it is important to take note.

|

These things are hard to call, and being primarily a value investor, I should not be making judgements at macro level. However, high valuations make me uncomfortable, and the expectation of unrelenting double digit revenue/profit growth for AI related companies as far as eye can see in the future, tempts me to take the other side of the trade.

|

Fortunately, I do not short stocks.

|

There are catalysts that can pop the bubble. Below are the few I see today:

|

- There will be delays and postponing of some data center projects due to funding issues or soft demand

- Hyperscalers are on a construction binge which is fueled by debt. This cannot last. Debt will get expensive to issue as credit quality deteriorates and interest rates start going back up.

- Inflation exists and trying to mask it now only means that when it cannot be hidden, it will be already too late to do anything about it

- Enterprise users of AI have not seen paybacks yet. Eventually they will, but time has a curious way of tempering enthusiasm and the investors will cool on how high multiples they are will to pay for these stocks

- There will be shortages of critical precious metals. Silver is being throttled by China, and it is a key component of GPUs. Silver is also a key component of EV solid state batteries.

- And then there is the global political environment. It is important for us investors to observe and plan for how these may play out.

All in all I believe some cash today is prudent. You may wish to maintain a reasonable amount of cash or cash equivalents (short term treasuries, CDs, etc) outside of this portfolio.

|

2026 promises to be a year where discipline and valuations will matter more than ever. As prudent investors, we have the edge.

|

|

Have a most profitable year.

|

|

|

|

|

|

|

|

|

|

|

|

|

Inner Circle Portfolio Performance

|

|

|

|

The portfolio performance is updated once a month, and tracked YTD until the end of the prior month. Performance is tracked as time weighted total return.

|

|

|

|

|

|

Upgrade to Inner Circle

- My actual Small Cap Value portfolio with highly profitable but under followed stocks and Kelly Criterion optimized weights

- Detailed investment thesis for portfolio stocks, including target prices and expected returns emailed to you as soon as published

- 1 year membership with NO auto-renewal. Repurchase membership again if you wish to continue for another year once your term completes.

|

|

|

|

|

|

|

|

|

Net-Net Stocks in 2026: Are Graham's Deep Value Criteria Still Findable?

|

|

|

|

Benjamin Graham made his career finding them. Warren Buffett called them the most reliable source of investment returns he ever found. And virtually every serious value investor has, at some point, asked the same question I asked when I first discovered them: why isn't everyone doing this? Net-net stocks, companies trading below their net current asset value, are one of …

|

|

|

|

|

|

|

|

Piotroski F-Score in Practice: How I Use It to Confirm a Value Pick

|

|

|

|

I want to be upfront about something: I do not use the Piotroski F-Score as a primary stock screen most of the time. That might surprise you, given how much ink gets spilled on Piotroski scores in value investing circles. But my process is different: I use it as a confirmation tool, not a discovery tool. Most of the cases, …

|

|

|

|

|

|

|

|

Managing Drawdowns: How I Protect Capital Without Losing Upside

|

|

|

|

In 2008, one of my portfolio positions fell 67% in four months. I had bought a small industrial company with a clean balance sheet, a long operating history, and what I thought was a conservative valuation. Then the financial crisis hit, credit markets froze, and customers stopped ordering. The stock went from $18 to $6 in the time it takes …

|

|

|

|

|

|

|

|

|

|

|

|

|