|

|

|

|

|

|

|

|

Portfolio Construction vs. Stock Selection (Where Most Investors Go Wrong)

Walk into the investing section of your favorite bookstore and look around.

|

You will find countless books about how to pick the right stocks. There may be variations on the theme. For example, some books will teach you to analyze stocks using fundamentals. Some will teach you how to time the stocks using technical analysis. There are books on trend following that lay out in great detail how to find stocks with momentum, when to get on and when to get off.

|

As a result, a significant proportion of retail investors believe that successful investing depends on finding the right stocks.

|

The financial media encourages this with articles like "Top 10 Stocks to Buy Now", or "What is Buffett Buying or Selling Today". There are 1000s of newsletters on the internet today that all promise to give you the perfect stock.

|

Here is the problem. No denying the fact that there is merit in a lot of the advice on stock picking. Also, you will find some great stock ideas in this process. But stock picking is just a small contributor to your investment results. In reality, portfolio outcomes are dominated by how the portfolios are constructed and managed.

|

Why Stock Selection Is Overemphasized

People love success stories. Whether it is at work, or at the neighborhood bar, you have seen investors joyfully recounting how a certain stock doubled or tripled and made them thousands or millions of dollars in very short order.

|

These stories are seductive.

|

You hear someone hit the jackpot once, and you may envy their luck. If this person has a string of winners, you might wonder what skills they have in finding great stocks, and you would be happy to invite them to dinner to exchange war stories.

|

When money is involved, we get our emotions vested in the outcomes. And the outcomes that have well defined hero - such as an outstanding stock pick - stick in our mind more than a steady relentless compounding.

|

Media sells more copies when there are stories of great performing stocks. Social media influencers have bigger following when the hits keep coming on their feed. It is just human nature to focus on the shiny stuff more than the dull stuff.

|

What are generally lost in these narratives are things like

|

-

|

The stock went 10X but sadly I only had a very small portion of the portfolio in it, so I am not rich yet,

|

-

|

This stock was one of the stocks I listed as top buys - I didn't really buy it,

|

-

|

Other stocks in the portfolio did not do well so overall I am still losing money,

|

-

And you rarely pay attention to people who tell you that all their stocks were good to solid, but the portfolio beat the market and has done so consistently year after year.

|

Remember, being right on a a few stocks does not guarantee portfolio success. There are several other aspects of investing that add to your great stock picks to help create a successful portfolio.

|

What Portfolio Construction Actually Means (and What It Is Not)

|

A well constructed portfolio gives you a whole that is greater than sum of its parts. Each component of the portfolio has a reason to be in the portfolio. I like to say that not every good stock should be bought. You only buy stocks that adds to your portfolio. Do not buy a stock that brings redundancies, or even make your portfolio weaker, no matter the merits of this individual stock.

|

Diversification is important. But diversification is not the same as buying 500 companies. This will make your portfolio average, and average is not something you should aspire to. There is a smarter way to structure your portfolio.

|

A well constructed portfolio should do the following:

|

-

|

Made up of largely uncorrelated assets. This reduces volatility for the portfolio, but it also adds additional alpha in terms of rebalancing bonus. See #2 below

|

-

|

Positions should be sized intelligently. When the prices change and the allocations drift, the portfolio should be rebalanced to bring it back to the optimal position sizes. There are different ways to position size: Kelly Criterion helps you optimize for performance, while a Risk Parity system sizes every position to equalize risk contribution to the portfolio.

|

-

|

While equal weighting is one way to size positions, it is not ideal to manage risk or maximize performance.

|

-

|

Your position sizing system should ideally consider the correlations between the assets in the portfolio, so you do not inadvertently over expose your portfolio to any one risk factor.

|

-

|

Finally, markets change and the economic conditions change, sometime rapidly. Your primary responsibility as an investor is to survive ALL market stresses. Your portfolio structure should give you this resilience.

|

The last point is very important. If you get wiped out, you set back the compounding by years. And you will get wiped out if you get too aggressive. On the other hand, if you are too defensive, your performance will suffer. There is an optimal level of aggressiveness that maximizes the long term growth of your portfolio. How you construct your portfolio will decide where you are on this spectrum.

|

How Good Stock Pickers Still Fail

Suppose you have utmost conviction in one particular stock, and you borrow money and bet it all. Eventually you are proven right and if you had been able to hold on to the stock, you would have made out handsomely.

|

Unfortunately, margin calls zeroed out your portfolio before you could retire.

|

Great stock pickers do not always build great wealth. Some do, of course, but only when they have figured out the hidden failure modes and taken steps to avoid them. These failure modes include: oversized conviction positions, unintentional factor concentration, neglecting correlations during drawdowns, and letting winners or losers dominate the portfolio.

|

These failures occur, even when the stock analysis is sound.

|

The Asymmetry Between Selection Skill and Construction Skill

There is an inherent contradiction between stock selection and portfolio construction. When you are picking stocks, you are looking for the possibility of maximal performance. You recognize that there are risks, but your focus is entirely on the pot of gold at the end of the investment journey. Why else would you invest in this stock?

|

When you construct your portfolio, you start paying attention to risk. Specifically risk of ruin. You want the pot of gold but you also realize that you have to be able to survive and stay on the path to eventually get there.

|

There is a constant conflict between risk taking and risk averse natures of these 2 skills. Fortunately, a construction first mindset does not mean you have to give up on the potential profits. Not at all.

|

What a Construction-First Mindset Changes

A construction first mindset means you realize that to win the game, you have to stay in the game. Survival is a pre-requisite to wealth.

|

Here is how your mindset changes. You stop asking "is this a great stock?" and start asking "what role does this stock play in my portfolio?". You think in terms of exposure and not just individual ideas. And you care more about managing your drawdowns and less about bragging rights (of maybe finding a unicorn stock).

|

You may have heard some say that good investing is meant to be boring. This does not necessarily mean that you need to buy stodgy boring companies to be a good investor. What it means is that good investing is a process, a journey. It is not a highlights reel.

|

Why This Matters Even More in Small-Cap Value

Small cap value. The asset class that has been shown again and again to be the asset class that beats all other asset classes for risk-adjusted returns. It is also the asset class that most investment advisors and financial planners will suggest you avoid.

|

If you do not have a process and a focus on portfolio construction, investing in small cap value can hurt you instead of rewarding you. Small caps amplify both mistakes and discipline. You could get away with a bad stock selection in large cap universe, but in small cap universe your margin of error is small. Small caps are also more volatile, which means that a poorly constructed portfolio can lead you to ruin quickly. A well constructed portfolio with some discipline will reward you well.

|

|

Without structure, small cap value becomes uninvestable for most people. This is why a large number of advisors do not recommend investing in small cap value.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

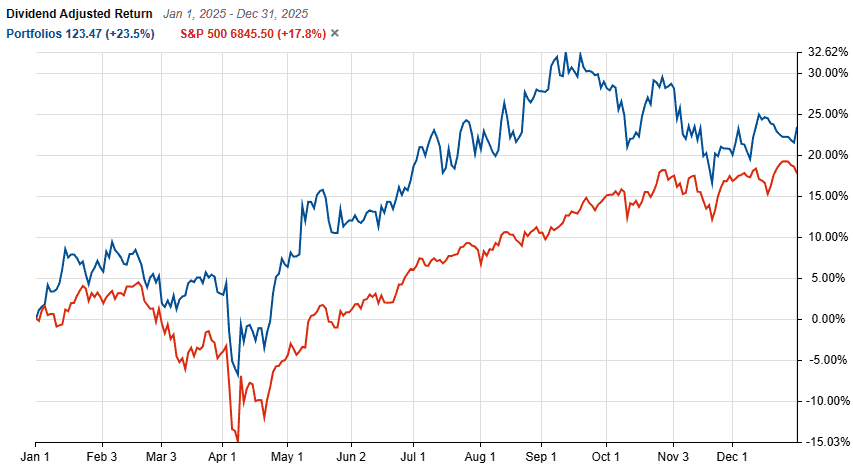

Inner Circle Portfolio Performance

|

|

|

The portfolio performance is updated once a month, and tracked YTD until the end of the prior month. Performance is tracked as time weighted total return.

|

|

|

|

|

|

Upgrade to Inner Circle

- My actual Small Cap Value portfolio with highly profitable but under followed stocks and Kelly Criterion optimized weights

- Detailed investment thesis for portfolio stocks, including target prices and expected returns emailed to you as soon as published

- 1 year membership with NO auto-renewal. Repurchase membership again if you wish to continue for another year once your term completes.

|

|

|

|

|

|

|

|

|

Net-Net Stocks in 2026: Are Graham's Deep Value Criteria Still Findable?

|

|

|

|

Benjamin Graham made his career finding them. Warren Buffett called them the most reliable source of investment returns he ever found. And virtually every serious value investor has, at some point, asked the same question I asked when I first discovered them: why isn't everyone doing this? Net-net stocks, companies trading below their net current asset value, are one of …

|

|

|

|

|

|

|

|

Piotroski F-Score in Practice: How I Use It to Confirm a Value Pick

|

|

|

|

I want to be upfront about something: I do not use the Piotroski F-Score as a primary stock screen most of the time. That might surprise you, given how much ink gets spilled on Piotroski scores in value investing circles. But my process is different: I use it as a confirmation tool, not a discovery tool. Most of the cases, …

|

|

|

|

|

|

|

|

Managing Drawdowns: How I Protect Capital Without Losing Upside

|

|

|

|

In 2008, one of my portfolio positions fell 67% in four months. I had bought a small industrial company with a clean balance sheet, a long operating history, and what I thought was a conservative valuation. Then the financial crisis hit, credit markets froze, and customers stopped ordering. The stock went from $18 to $6 in the time it takes …

|

|

|

|

|

|

|

|

|

|

|

|

|