|

|

|

|

|

|

|

|

Rebalancing, Volatility, and Return Harvesting

The traditional definition of risk is based upon volatility. Expressing volatility as risk implies that volatility is inherently bad, and something to avoid at all cost.

|

Seasoned investors will tell you that this is not true, no matter what the academics say.

|

Volatility is not risk. You should not avoid it at all costs. Volatility can in fact be an opportunity, if you handle it properly.

|

Why Volatility Feels So Uncomfortable

Absent any trigger (earnings, company news, etc.), the daily stock price movement of a stock is close to being random. However, since it involves our hard earned money, we cheer every time the stock price goes up, and we react emotionally when the price goes down.

|

Humans experience losses asymmetrically. Losses hurt more than gains bring us joy. This is why volatility stings. The media is no help - they amplify the ups and downs to get your attention. The daily stock market noise will affect your long term thinking if you are not disciplined enough to tune out the cacophony.

|

What Rebalancing Actually Does

You probably rebalance your portfolio periodically. This is an advice you will hear from experts and many have accepted this as sound advice. There is still some confusion around the nature of rebalancing and the benefits it brings to your portfolio.

|

Rebalancing involves selling parts of the stocks that have appreciated and using the proceeds to increase your holding in the stocks that have declined. This may imply that this is a market timing device. It is not. Rebalancing is a mechanical act performed on a schedule (or when certain pre-defined criteria is met), and it does not depend on market conditions or stock specific information. It is not intended to predict future performance, neither does it promise higher performance.

|

|

Rebalancing is a response to the drift in your portfolio. You use this process to reset the risk to the levels you are comfortable with, and it allows you to do this without needing to forecast the future.

|

That being said, rebalancing does offer performance advantages.

|

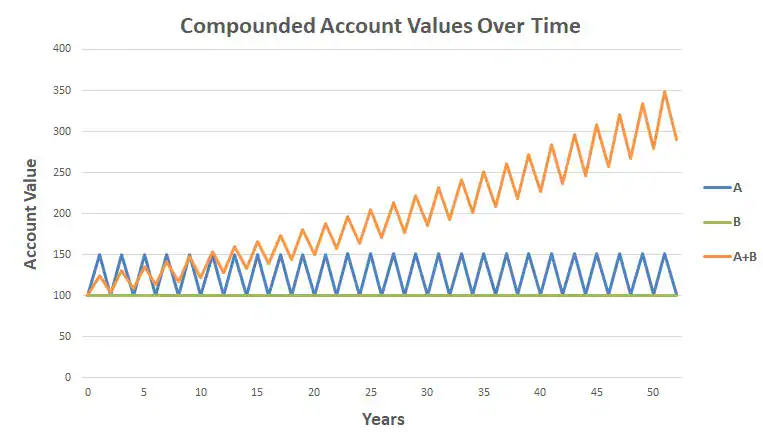

How Volatility Becomes a Source of Return

Systematic rebalancing converts fluctuation into incremental advantage. Stocks spend most of their time sitting outside of a trend - they are neither actively rising or actively declining. The volatility means the price does fluctuate. When you systematically rebalance, you take a little off when the price has spiked up, and add a little more when the price has spiked down.

|

The dollars you harvest by rebalancing when the stock has spiked up will buy larger number of shares when you reinvest when the stock price has spiked down.

|

This is a small increase in your holding size. But when you perform this action repeatedly, over time this small increase starts to compound. As a result, your portfolio grows faster than if you had not rebalanced at all.

|

Please note that this is not a guarantee. A stock that is in strong uptrend is better left alone until the momentum behind the stock tapers off. For long term investors it is important to note that uptrends (and downtrends) last for a short time. Most of the time the stock is in a plateau. Rebalancing helps you get returns during the time when the "stock is not going anywhere" by harvesting volatility.

|

Why Rebalancing Matters More in Small-Cap Value

Small cap stocks exhibit larger swings, and therefore there is more volatility to be harvested. Value stocks tend to sit in the purgatory for longer as investor attention is not on the stock, therefore the time window to harvest volatility is larger as well.

|

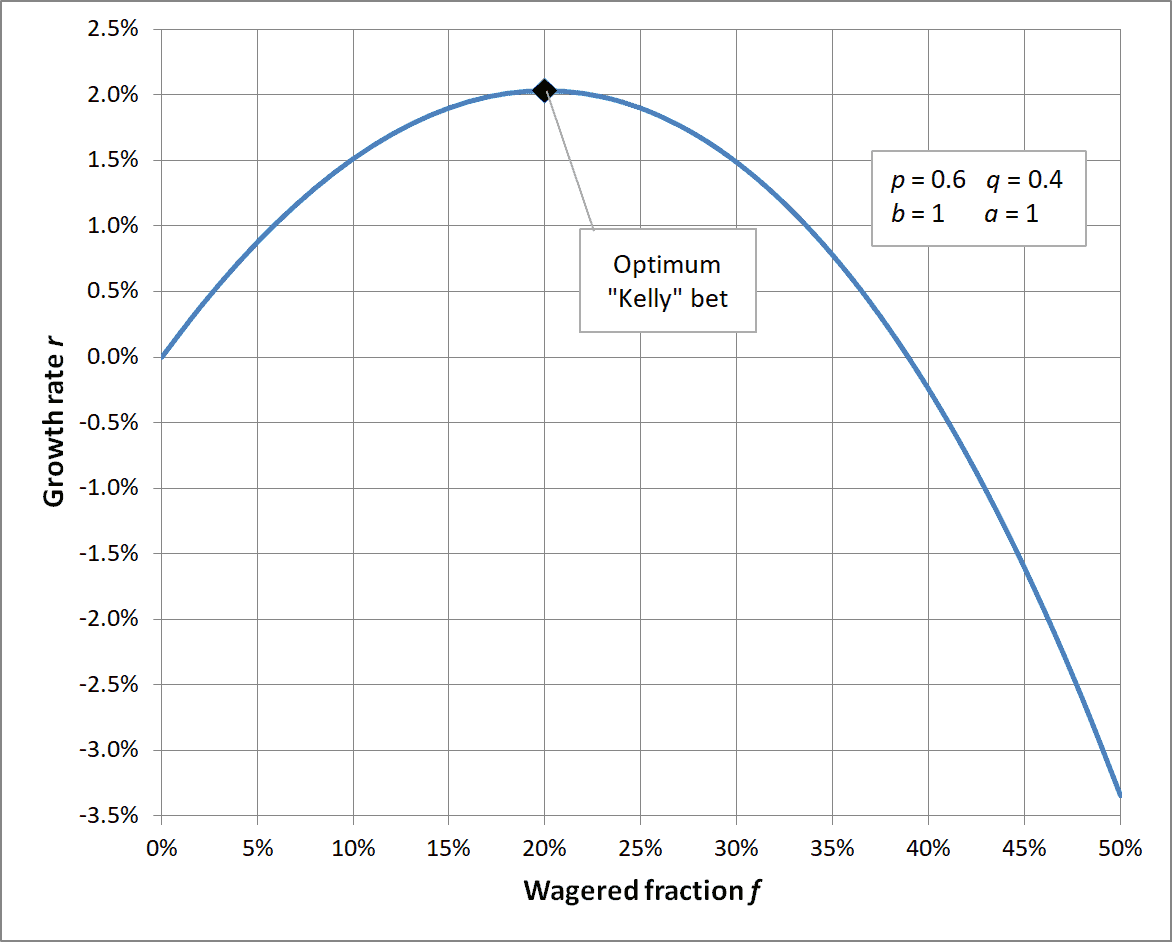

Additionally, if you use Kelly Criterion or some other method to size your positions, rebalancing ensures that your portfolio stays aligned with your optimal allocations. This way, when the value realization occurs, you know you have maximized your performance.

|

The Cost of Not Rebalancing

What if you don't rebalance? Many value investors are on the record saying they do not believe in rebalancing. They are wrong.

|

First of all, rebalancing allows you to continuously reduce your cost basis and acquire more shares of the stocks you find undervalued. As value investors, this is excellent and I see no reason to give up this advantage. But there is a more critical problem. Let me explain.

|

Say you buy a stock that is trading at a 30% discount to the fair value and the stock price has risen so the discount now is only about 10%. The stock is still undervalued, but from this point on your expected returns are smaller while your allocation is much larger. This means you are now taking unnecessary risk to earn smaller reward.

|

The ideal solution is to recalculate your position sizing and then rebalance to it. This can be some work. However, if you merely rebalance your portfolio to original weights, you still reduce your risk by reducing the concentration of the stock in your portfolio.

|

Remember, most of your long term returns come from the risks you eliminate.

|

Foundational Reading

|

|

|

|

|

|

|

|

|

|

|

|

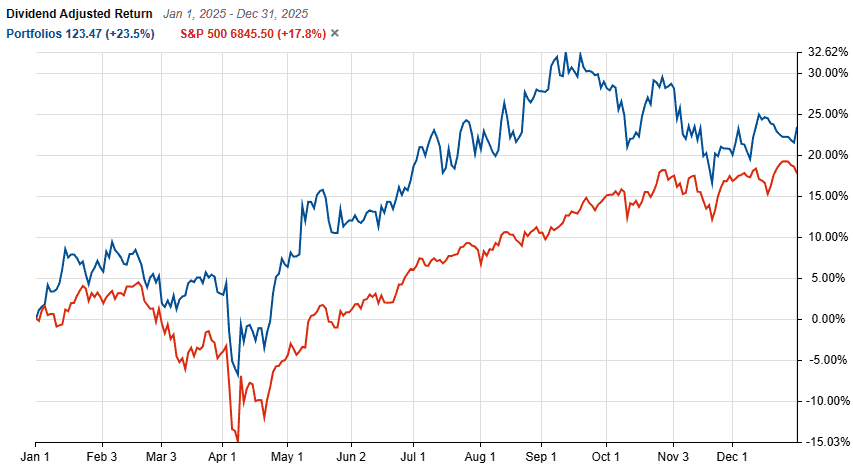

Inner Circle Portfolio Performance

|

|

|

The portfolio performance is updated once a month, and tracked YTD until the end of the prior month. Performance is tracked as time weighted total return.

|

|

|

|

|

|

Upgrade to Inner Circle

- My actual Small Cap Value portfolio with highly profitable but under followed stocks and Kelly Criterion optimized weights

- Detailed investment thesis for portfolio stocks, including target prices and expected returns emailed to you as soon as published

- 1 year membership with NO auto-renewal. Repurchase membership again if you wish to continue for another year once your term completes.

|

|

|

|

|

|

|

|

|

Managing Drawdowns: How I Protect Capital Without Losing Upside

|

|

|

|

In 2008, one of my portfolio positions fell 67% in four months. I had bought a small industrial company with a clean balance sheet, a long operating history, and what I thought was a conservative valuation. Then the financial crisis hit, credit markets froze, and customers stopped ordering. The stock went from $18 to $6 in the time it takes …

|

|

|

|

|

|

|

|

Shannon's Demon Explained: Why Rebalancing Beats Buy-and-Hold Over Time

|

|

|

|

I want to tell you about one of the most counterintuitive ideas in all of investing, an idea so strange that when I first encountered it, I spent about an hour with a spreadsheet trying to convince myself it was wrong before I finally accepted that it was right. It is called Shannon's Demon. And once you understand it, you …

|

|

|

|

|

|

|

|

Full Kelly vs. Fractional Kelly: Which Position Sizing Approach Is Right for You?

|

|

|

|

Most investors spend enormous effort deciding which stocks to buy and almost no effort deciding how much to buy. That is exactly backwards. In the long run, position sizing will have as much impact on your returns as stock selection and it will have more impact on your survival as an investor. I use the Kelly Criterion as the mathematical …

|

|

|

|

|

|

|

|

|

|

|

|

|